Call to protect HR 676, the model single payer bill. Patients not profits!

Serious attempts are being made to undermine HR 676 by removing the ban on investor-owned, for-profit hospitals, nursing homes, and other institutions. This effort to gut HR 676 is being done in the face of multiple studies showing that private for-profit hospitals and other facilities have higher costs and produce poorer outcomes.

A recent article by two prominent health policy researchers on the influential Healthcare Affairs website looks at just how much it might cost to remove all for-profit entities from the healthcare system under HR 676 and concludes that it might even save money.

Below we reproduce that portion of the article that examines the removal of investor-owned hospitals and other for-profit facilities. We urge you to call Congresswoman Pramila Jayapal’s office (202) 225-3106 and tell her to protect HR 676 by keeping the ban on for-profit hospitals and other facilities. Patients not profits.

https://www.healthaffairs.org/do/10.1377/hblog20181116.732860/full/

The Future Of Investor-Owned Care

The House single-payer bill envisions a buyout of the investor-owned facilities needed to provide care under the single-payer system, while the Senate version would leave them in current hands.

Proponents of the House approach acknowledge that many non-profit health care organizations have drifted far from their charitable roots. However, they cite evidence that for-profit providers (including hospitals, dialysis centers, nursing homes, home care agencies, and hospices) provide inferior care at inflated prices (see, for instance here, here, here, here and here) and are more likely to bend care to profitability (see here, here, here and here). For-profit hospitals spend less on nurses and other clinical aspects of care, but more on administration and financial management; for-profit chains have often been cited for questionable business practices and have been repeatedly implicated in large scale fraud (see here, here, here and here).

According to CMS, for-profit nursing homes are cited for quality deficiencies 28 percent more often than non-profits, and for deficiencies that place residents in immediate jeopardy 53 percent more frequently. Investor-owned home care agencies cost Medicare $752 more per patient than non-profit agencies, while providing worse care.

Yet even some who would prefer to exclude investor-owned facilities from a single-payer system worry about the cost of a buyout. In conversations with Congressional aides, some have suggested that these costs could amount to $1 trillion or more, although none could cite a source for that figure. While it’s not clear exactly how to value the assets of investor-owned medical facilities, estimates of their current capital assets and of their stock market valuations provide some guidance.

In the detailed cost reports filed with Medicare covering fiscal year 2016 (the most recent year for which virtually all reports are available), all for-profit hospitals taken together reported total capital assets of $97.845 billion at the start of the year, and additional purchases totaling $7.453 billion (Himmelstein & Woolhandler, unpublished analysis of hospital cost reports). So the total capital stock of all for-profit hospitals - including not just acute care hospitals, but most other inpatient facilities besides stand-alone nursing homes - totaled $105.298 billion. (The comparable figure for non-profits is $718.628 billion).

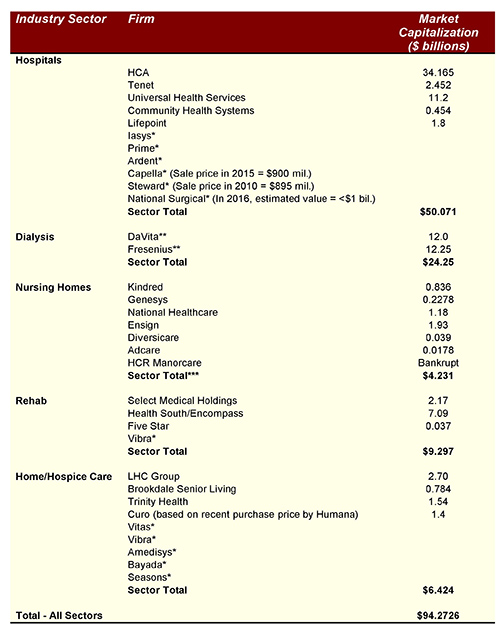

Since most investor-owned providers also carry debt, it’s not surprising that the capital asset figures are considerably higher than the stock market value of the firms that own the facilities. As indicated in Exhibit 1, the market valuation of the five publicly-traded firms that account for the vast majority of for-profit hospitals totals $50.071 billion. While data on the market value of the (smaller) privately held for-profit hospital chains is not available, the value of the larger chains, and past sale prices for three of the privately-held firms, suggests that they’d add only several billion to the total.

Exhibit 1: Market Value Of Investor-Owned Health Care Providers

Source: Health Affairs

Notes for Exhibit: Figures for market capitalization for firms that are included in the Fortune 500 were taken from Fortune June 1, 2018. Other figures are from Google Finance and other online sources, searched October 26, 2018.

* Privately-held firm, no market capitalization or recent sale price data available

** Figures include value of dialysis supply business as well as health service delivery. Fresenius figure is adjusted for share of business in U.S.

*** Figures for some nursing firms include value of senior living communities

Similarly, as Exhibit 1 shows, the total value of shares in publicly traded nursing home firms, rehab, dialysis, and home care and hospice providers is relatively modest: less than $50 billion. And these valuations (which fluctuate from day-to-day) include aspects of the businesses that would not be included in a buyout, e.g. the value of real estate devoted to senior living communities, or the roughly 15 percent of DaVita’s business that’s unrelated to dialysis and the 20 percent of Fresenius’ revenues attributable to sales of products such as dialysis supplies.

Overall, the fair market value of investor-owned facilities covered by a buyout, whether assessed by capital stock or stock prices, seems unlikely to exceed $150 billion. Purchasing these assets using Treasury Bill financing over 15 years at the current interest rate of 3 percent would cost about $12.75 billion annually, equivalent to about 1 percent of annual hospital costs. Moreover, even in the short term, some or all of these costs would be offset by savings on profits, which totaled more than $6 billion in 2017 for just three of these firms (HCA, DaVita and Fresenius).

Bottom line: A buyout of investor-owned facilities is affordable. Indeed, it might well lower costs.

11/30/2018